Share this

by Juan Gutierrez and Thomas Haas on Sep 19, 2022 10:30:00 AM

Introduction

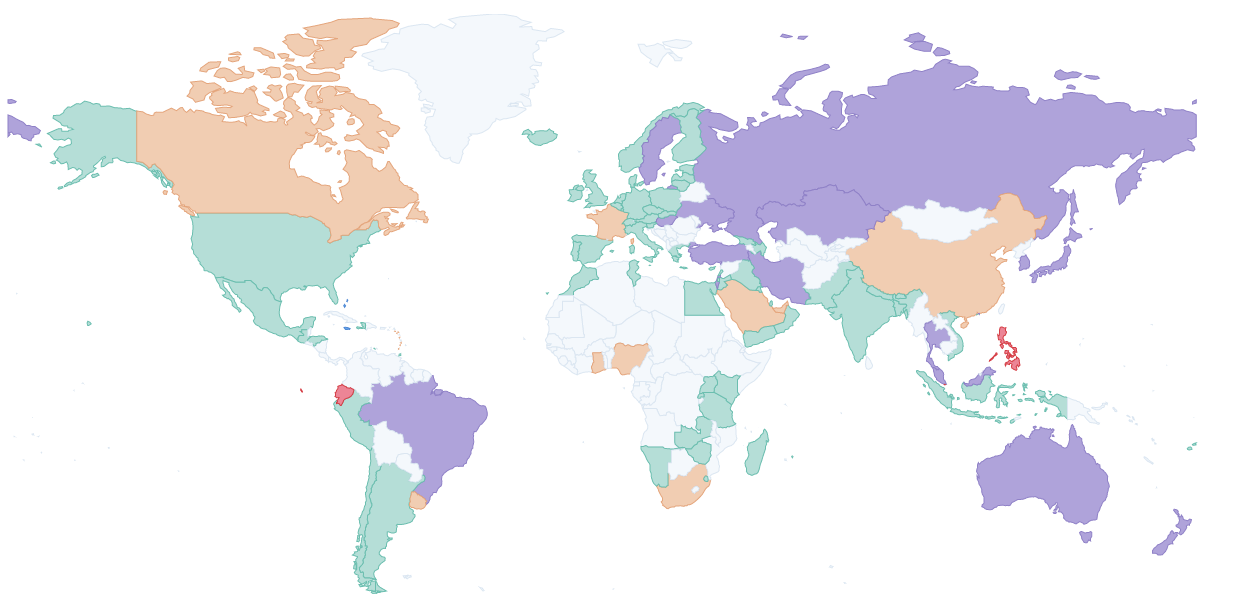

Central bank digital currencies (CBDCs) have evolved in just a few years from a purely academic discussion to an intense debate among central banks around the world about the future of public and private digital money. As of 2022, most central banks are at least conducting research on CBDCs, several have launched development projects and pilots. (Figure 1).

Figure 1: Global CBDC Tracker as of August 2022

(Source: cbdctracker.org)

This article is the first in a series that highlights the current state of international CBDC projects, with a selection of several representative efforts. This first article provides a general overview of global CBDC projects, motivations, and goals in the following countries:

- China

Its digital yuan pilot is one of the longest large scale CBDC efforts. It also draws attention due to how advanced its private digital money providers are and its potential role in an international expansion of the renminbi. - Eastern Caribbean States, Bahamas and Nigeria

These countries have already launched a CBDC or are in an advanced phase of a pilot. Even if they are relatively small, they can still provide lessons on the practical challenges of officially launching digital versions of their public money. - Russia

Since at least the annexation of the Crimean Peninsula in 2014, Russia has been under international sanctions. As a result, it has taken several steps to retain its monetary sovereignty and reduce its dependence on foreign payment structures. There have been discussions about whether the digital ruble pilot, which was already relatively advanced before the invasion of Ukraine, is part of this effort.

The remainder of this article is organized as follows: Section 2 provides an overview of the international work on CBDCs, Section 3 discusses the objectives and rationale for central bank engagement with CBDCs, and Section 4 concludes this CBDC overview article.

International work on CBDCs

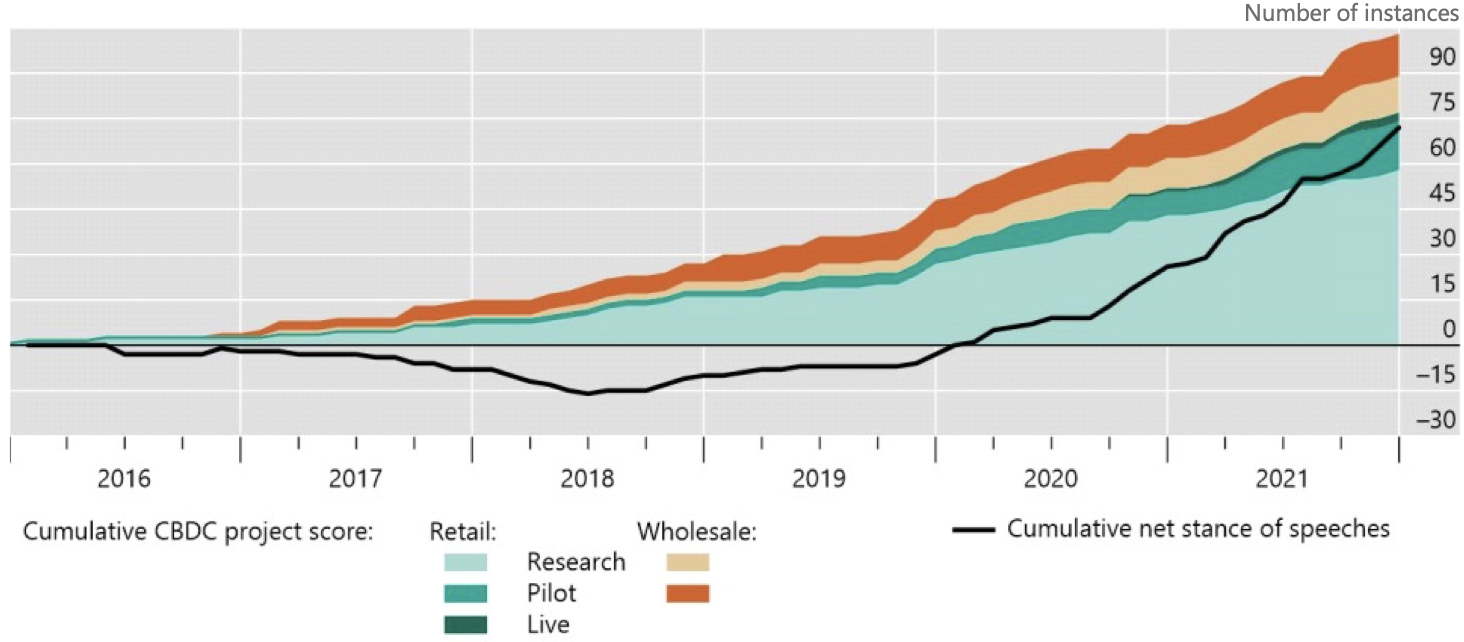

Central bank engagement in CBDC work has increased sharply in recent years. While only a few central banks were working on CBDCs five years ago, there are now over 90 CBDC projects underway (Figure 2). While the majority of central banks are focused on retail CBDCs, there are also several wholesale CBDC projects. Figure 2 also shows that the net sentiment in central bank speeches has changed from negative in 2017 to positive in 2019.

Figure 2: CBDC projects

(Source: Auer et al. (2020))

Although central bank involvement in CBDC projects is increasing and their sentiment towards them is improving, central banks remain cautious about issuing CBDCs. In a 2020 survey of central banks, Boar and Wehrli (2021) showed that 60% of respondent central banks still considered that the issuance of a CBDC could take up to six years.

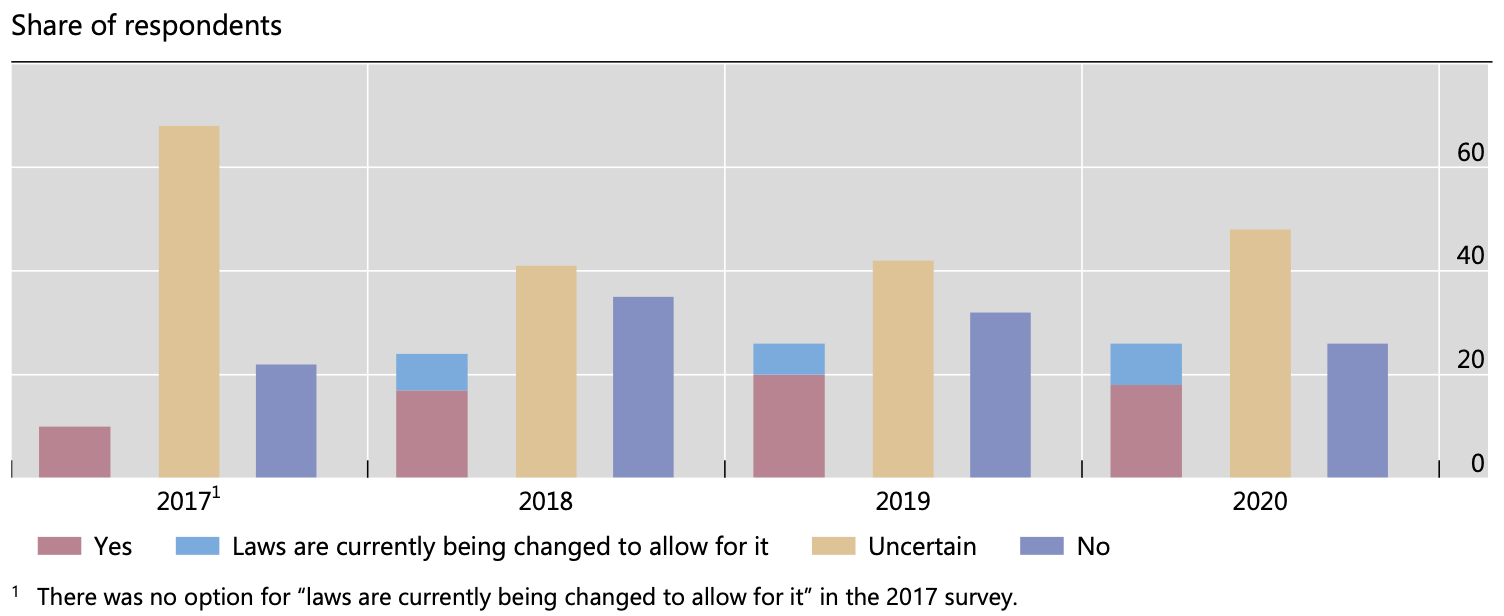

The crucial question of whether central banks have the legal authority to issue CBDCs also remains quite uncertain (Figure 3). In the latest release of the BIS survey of central banks on CBDC issuance, the share of respondents who were unsure about their legal authority to issue CBDCs was still around 50%. However, legislative changes are already underway in some countries to change the legal situation and allow central banks to issue CBDCs.

Figure 3: Legal authority of central banks to issue a CBDC

(Source: Boar and Wehrli (2021))

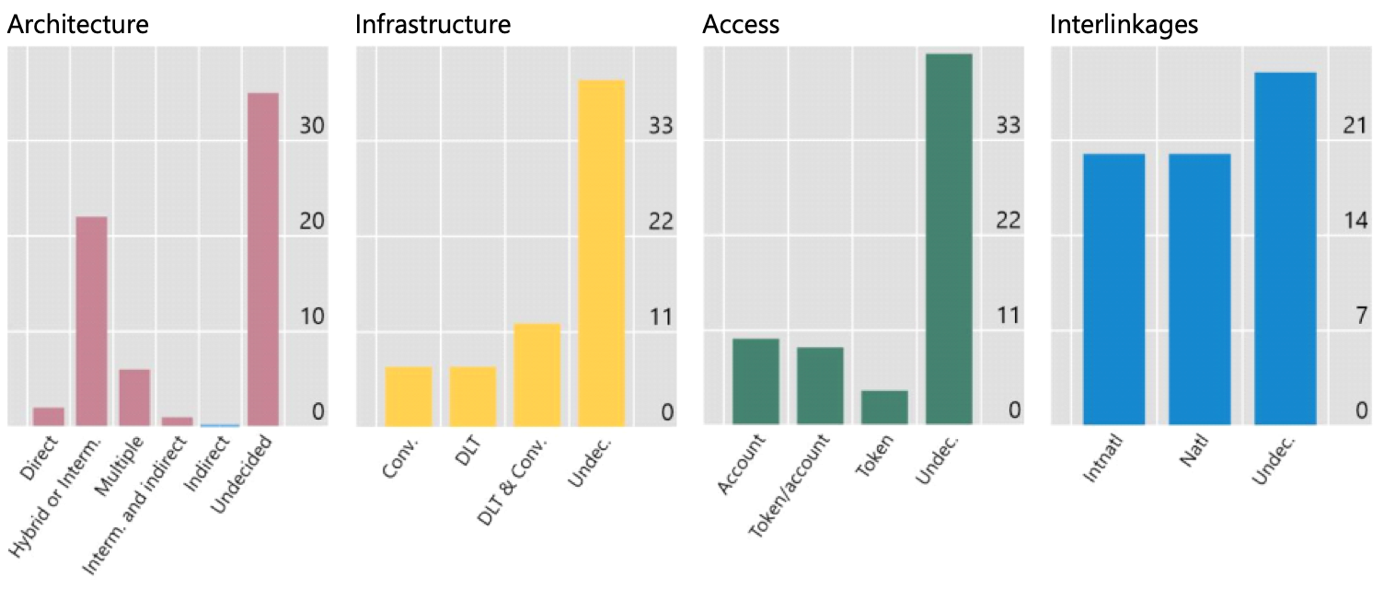

Central banks are also still largely undecided on the design of CBDCs. Figure 4 shows the status of central banks CBDC work in relation to the various design options in January 2022. The proportion of "undecideds" is the highest for all categories.

- Architecture - Most central banks opt for a "hybrid" or "intermediary" CBDC design, where CBDCs and the corresponding payments are handled by intermediaries (see, e.g., Auer and Böhme (2021) for a more detailed description).

- Infrastructure - There is a slight preference for a combination of conventional centralized and distributed ledger technology.

- Access - There is a slight preference for account-based systems over token-based systems or a combination of both.

- Interlinkages - There are about as many CBDC projects that would seek international use as there are ones that are focused on domestic use.

Figure 4: Number of retail CBDC projects investigating each design option

(Source: Auer et al. (2020))

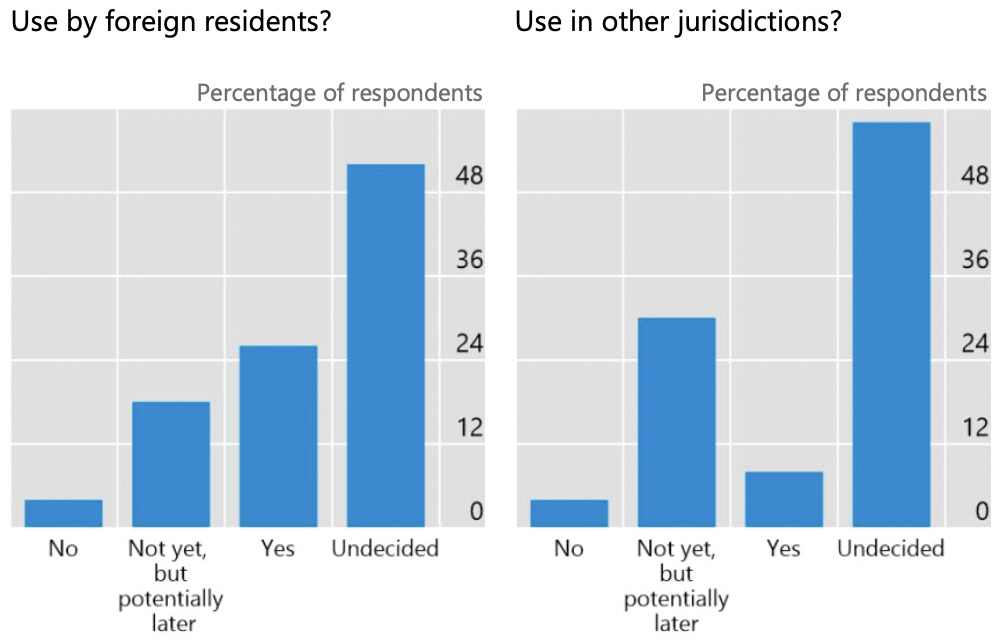

Most of the focus in CBDC projects and research has been on the domestic use of a CBDC. In recent years however, more attention has been paid to the issue of international use of CBDC and its implications for cross-border payments (see., Auer et al. (2021b), BIS (2021a), BIS (2021b), BIS (2022a), CPMI (2021), Demmou and Sagot (2021), Worldbank (2021a), Worldbank (2021b)). Figure 5 shows that, while most are still undecided, central banks tend to agree with granting non-residents access to their CBDCs but are more cautious about its use outside their respective jurisdictions.

Figure 5: CBDC likelihood of issuance

(Source: Auer et al. (2021a))

This cautious approach is mainly motivated by fears of international spillover effects (Ferrari et al. (2020)), currency substitution (IMF (2020)), tax avoidance, or a loss of domestic supervisory capabilities (Auer et al. (2021a)). While these risks need to be addressed, CBDCs are also seen as a tool to address existing problems in cross-border transactions, such as high costs, low speed, limited access, and limited transparency (e.g., Worldbank (2021b)).

Goals and motivations of CBDC

Boar and Wehrli (2021) show that domestic payment efficiency and payment security are the most important motivations for central banks in advanced economies to consider issuing a CBDC (figure 6). For central banks in emerging economies, financial inclusion and domestic payment efficiency are the most important motivations.

Figure 6: Motivations for issuing a retail CBDC

(Source: Boar and Wehrli (2021))

Other motivations and policy objectives for issuing CBDCs include (e.g., Kiff et al. (2020), Bindseil et al. (2021)):

- the declining importance of cash in payments

- the risk of a wide adoption of new forms of private money such as stablecoins

- improving monetary policy transmission

- preserving monetary sovereignty and strategic autonomy

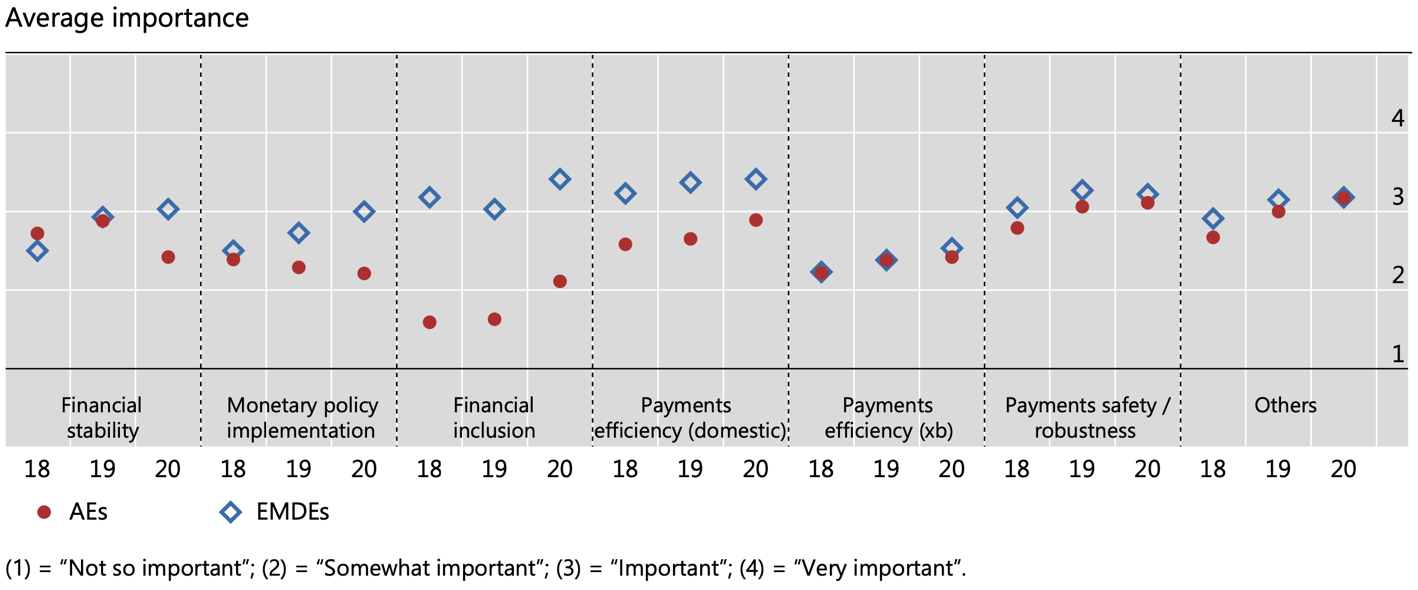

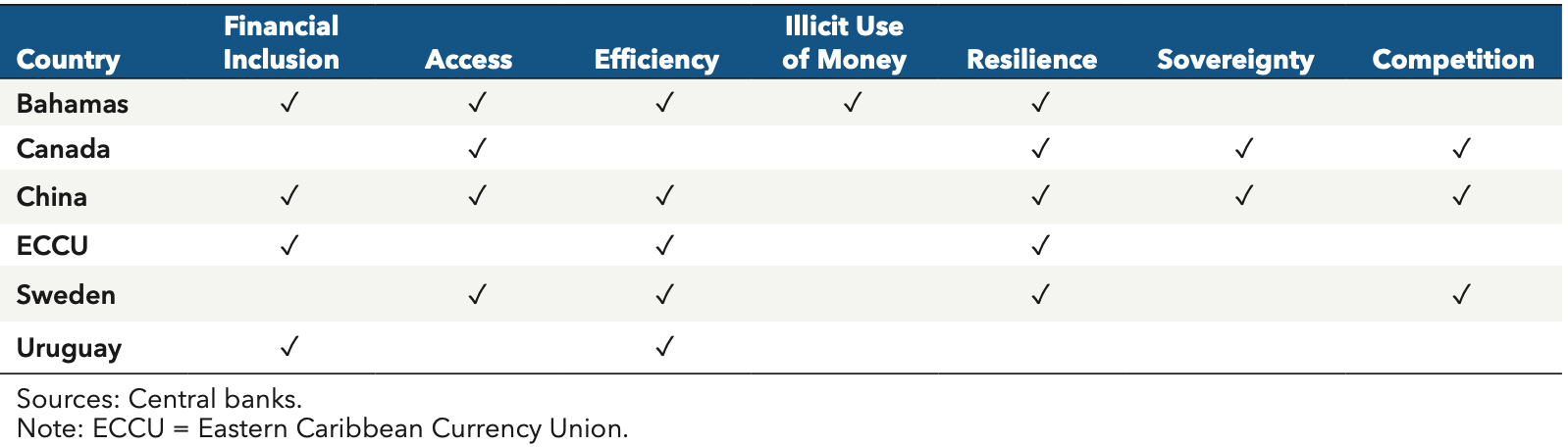

In a recent publication, the IMF (2022) discussed CBDC projects in various countries. Figure 7 shows the respective policy objectives of these six pilot examples.

Figure 7: Jurisdictions’ Stated Policy Goals of Central Bank Digital Currency

(Source: IMF (2022))

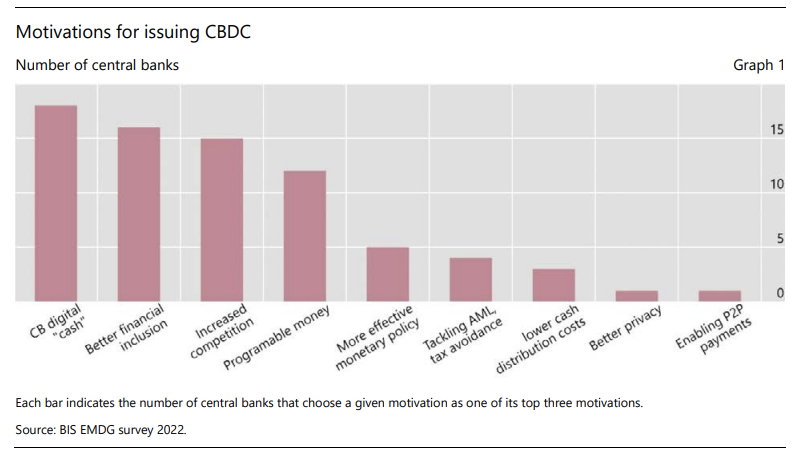

In a set of papers prepared for a meeting of 26 central bank governors, the BIS (2022b) found that providing a “CB digital cash” was also a top priority for emerging central banks and there was also greater interest in “programmable money” (Figure 8).

(Source: BIS (2022b))

There is a difference in the approach and policy objectives of central banks in emerging or developing economies, and advanced economies related to CBDCs. Emerging or developing economy central banks focus on financial inclusion and access to an efficient and resilient payment system. These central banks have recently given greater importance to providing digital cash and programmable money.

Advanced economy central banks place more emphasis on preserving sovereignty and ensuring competition in the payment system. In the most recent survey presented, advanced economy central banks have slightly reduced the priority of financial stability and monetary policy implementation and increased that of financial inclusion.

Although there are significant coordination efforts among all central banks to avoid international spillover effects such as currency substitution from private or public money providers, there is also a consensus on the need to continue to seek improvements on cross-border payments.

Conclusion and digital euro implications

This introductory article shows that while most central banks have been actively engaged in CBDC research and projects for several years and, have had on average, a positive attitude towards them since at least 2020. It is clear though that central banks are still defining design options and committing to the issuance of a retail CBDC. Central banks will likely require more research to advance into pilots and learn from other CBDC “go-lives'' to settle on their specific take on the fundamental design tradeoffs.

There is a structural difference in CBDC work between central banks in developing economies and those in advanced economies. This is particularly the case with respect to financial inclusion which is a higher priority for develop[ing economies. Over time, the relative importance of financial stability and monetary policy implementation seems to have fallen slightly for advanced economies, while digital cash and programmable money seems to have grown for emerging and developing economies.

Most central banks have allocated their CBDCs for local use, including by foreign residents, but they are aware of the opportunities of CBDCs to improve cross-border payments and the potential risks to their monetary sovereignty, either from private monies, including global stablecoins, or from other CBDCs. Coordinated efforts on these international spillovers are ongoing. While there is a potential role for a CBDC to support a government’s expansion of the international role for its currency, and even to weaken the financial pressure applied to it through financial sanctions, there is at present no significant direct evidence of this from the CBDC pilots in Russia and China.

The European Central Bank (ECB) is currently in a two-year investigation phase set to end in 2023 with a decision on whether it will issue a digital euro. If the outcome is positive, the ECB will enter a development phase that would last about three years before a digital euro could be introduced (Panetta 2021).

A recent ECB-commissioned study on payment methods by Kantar Public (2022) shows that a new digital payment method can only generate interest and engagement and drive adoption if it offers "compelling advantages over current options or novel benefits that simplify daily life" (Kantar Public 2022, p. 6). This need to offer users a distinct advantage over existing solutions to drive adoption is also reflected in a consumer survey conducted by OMFIF (2021) and Giesecke + Devrient. The important task then for the ECB is to find a unique selling proposition that a digital euro could offer its users compared to the already highly developed and efficient payment landscape in the euro area (e.g., BIS 2021c).

The subsequent articles in this series will attempt to provide a deeper understanding of CBDC research and development in countries with different challenges and policy objectives. The articles will highlight that there is no one-size-fits-all approach to CBDC, but that CBDC solutions must be based on the needs and challenges of each country. Nevertheless, the international perspective and comparison of different CBDC initiatives provides valuable insights and lessons for the development and design of a possible digital euro.

References Introductory Paper:

Auer, R., Cornelli, G., & Frost, J. (2020). Rise of the central bank digital currencies: drivers, approaches and technologies. BIS working papers, No 880, updated January 2022.

Auer, R., & Böhme, R. (2021). Central bank digital currency: the quest for minimally invasive technology. BIS Working Papers, No. 948.

Auer, R., Boar, C., Cornelli, G., Frost, J., Holden, H., & Wehrli, A. (2021a). CBDCs beyond borders: results from a survey of central banks. BIS Papers, No. 116.

Auer, R., Haene, P., & Holden, H. (2021b). Multi-CBDC arrangements and the future of cross- border payments. BIS Papers, No. 115.

Bindseil, U., Panetta, F., & Terol, I. (2021). Central Bank Digital Currency: functional scope, pricing and controls. ECB Occasional Paper Series, No. 286.

BIS (2021a). Central banks of China and United Arab Emirates join digital currency project for cross-border payments, 23 February, https://www.bis.org/press/p210223.htm.

BIS (2021b). Multi-CBDC prototype shows potential for reducing costs and speeding up cross-border payments, 28 September, https://www.bis.org/press/p210928.htm.

BIS (2021c). Central bank digital currencies: user needs and adoption, September, https://www.bis.org/publ/othp42_user_needs.pdf.

BIS (2022a). Project Dunbar: international settlements using multi-CBDCs, https://www.bis.org/publ/othp47.pdf.

BIS (2022b) CBDCs in emerging market economies. https://www.bis.org/publ/bppdf/bispap123.htm

CPMI (2021). Central bank digital currencies for cross-border payments. July, https://www.bis.org/publ/othp38.htm

Boar, C., & Wehrli, A. (2021). Ready, steady, go? – Results of the third BIS survey on central bank digital currency. BIS Papers, No. 114.

Demmou, L. and Q. Sagot (2021), "Central Bank Digital Currencies and payments: A review of domestic and international implications", OECD Economics Department Working Papers, No. 1655.

Ferrari, M, Mehl, A., & Stracca, L. (2020). Central bank digital currency in an open economy. ECB working paper series, No. 2488, November.

IMF (2020). Digital money across borders: macro-financial implications. IMF Policy Papers, No 2020/050.

IMF (2022). Behind the Scenes of Central Bank Digital Currency: Emerging Trends, Insights, and Policy Lessons. IMF FinTech Notes, Note/2022/004.

Kantar Public. (2022). Study on New Digital Payment Methods. https://www.ecb.europa.eu/paym/digital_euro/investigation/profuse/shared/files/dedocs/ecb.dedocs220330_report.en.pdf

Kiff, J. Alwazir, J., Davidovic, S., Farias, A., Khan, A., Khiaonarong, T., Malaika, M., Monroe, H.K., Sugimoto, N., Tourpe, H., & Zhou, P. (2020). A Survey of Research on Retail Central Bank Digital Currency. IMF Working Paper, WP/20/104.

OMFIF (2021). Consumer attitudes to CBDC: Considerations for policy-makers.

Panetta, F. (2021). Preparing for the euro’s digital future. Blog post by Fabio Panetta, Member of the Executive Board of the ECB, July 14.

Worldbank (2021a). Central Bank Digital Currency : A Payments Perspective. World Bank Report, https://openknowledge.worldbank.org/handle/10986/36765

Worldbank (2021b). Central Bank Digital Currencies for Cross-border Payments : A Review of Current Experiments and Ideas. World Bank Report, https://openknowledge.worldbank.org/handle/10986/36764

This article was prepared by the authors. The views expressed in this article are the author’s own and do not necessarily reflect the views of the Digital Euro Association.

No Comments Yet

Let us know what you think