Share this

by Juan Gutierrez and Marlene Marz on Oct 24, 2022 10:15:00 AM

Introduction

According to the “Atlantic council CBDC tracker”, approximately 87 countries, representing over 90 percent of global GDP, are exploring CBDCs (Atlantic Council 2022). However, compared to the number of central banks researching this topic, very few have fully launched a CBDC or run an advanced pilot project. So far, the Bahamas (Sand Dollar) and Nigeria (e-Naira) operate a CBDC system, while the Eastern Caribbean Currency Union (ECCU) is running a pilot on most of its islands.

In this article, we take a closer look at how and why the Bahamas, Nigeria, and the ECCU managed to launch a CBDC in a relatively short period of time and how the projects have developed. For every one of the three presented CBDCs, there will be an introduction to outline the motivation for issuing a general purpose CBDC. Then, we will describe the design of the respective CBDCs, such as its technical basis; the involvement of the private sector, and any legal adaptations that had to be made. Then the three CBDC projects will be compared. The article concludes with possible findings for a potential digital euro.

Officially launched CBDCs

Bahamas

In October 2020, the Bahamas were the first country to nationally issue a modern CBDC (at least regarding DLT-based systems). The Central Bank of The Bahamas (CBoB) had been investigating CBDC since 2017. In December 2019, the digital version of the Bahamian dollar (B$) was first issued during a pilot in Exuma, one of the Bahamian islands (Cemla Fintech Forum, 2020). About ten months later, the CBDC was officially launched, requiring all merchants to accept payments in Sand Dollar (UN, 2019 / Sand Dollar, 2022).

Motivation

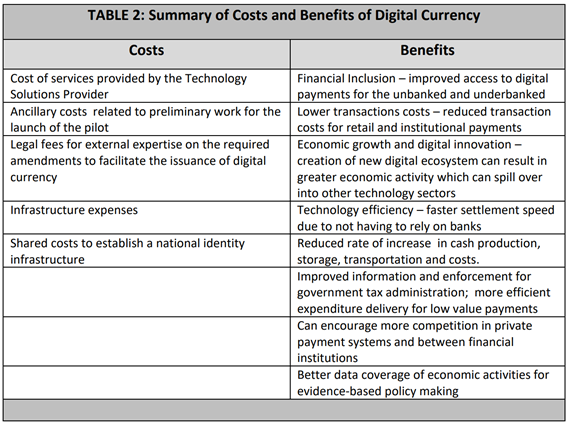

The issuance of the Sand Dollar is part of the Bahamian Payments System Modernization Initiative (PSMI), focusing on financial inclusion: “The Bahamian PSMI targets improved outcomes for financial inclusion and access, making the domestic payments system more efficient and non-discriminatory in access to financial services” (Central Bank of the Bahamas, 2019, p.3). See Figure 1.

Figure 1.

Potential Costs and Benefits (Central Bank of the Bahamas, 2019, p.22).

Furthermore, the CBoB describes the motivation as the following: “The main goals are that 100% of the population has access to digital payments services; universal access to banking services of a deposit account maintenance nature; a reduction in the size of legitimate but unrecorded economic activities that take place in the informal sector; and full admission of micro, small and medium-sized businesses into the digital space.” (Central Bank of the Bahamas, 2019, p.4)

CBDC-design

The Sand Dollar is designed as a retail CBDC, making payments in digital central bank money available for private households. The Sand Dollar is legal tender in the Bahamas. Its legal framework, such as governance and consumer protection standards, was published in mid-2020 (Sand Dollar Legal Framework 2020).

The Sand Dollar operates using a smartphone app and is issued by the Central Bank of The Bahamas through “Authorized Financial Institutions (AFIs)”. Customers may choose between these AFIs. It is possible to make payments via QR-code or a selected “Unique Custom Name” (Sand Dollar, 2022). The private sector (AFIs) is also responsible for registration and authentication of Sand Dollar users. The CBDC has tiered KYC requirements: Tier 1 accounts (basic customer information required) have a maximum holding limit of B$500 and a maximum transaction limit per month of B$1,500. Tier 2 accounts (Government-issued identification required) have a $8,000 eWallet holding limit, with a $10,000 monthly transaction limit. (Central Bank of the Bahamas, 2019, p.23).

Technical background and CBDC-adoption

NZIA was selected by the CBoB in March 2019 as technical partner for the digital Bahamian dollar (NZIA, 2019). The Sand Dollar is based on their “NZIA Cortex DLT”. The digital Bahamian Dollar was also the first CBDC to implement an offline payment function. In February 2021, the CBoB announced working together with Mastercard and the payment service provider Island Pay, to issue a Sand Dollar card (Mastercard 2021). This allows offline transactions from the app for registered users, and thus increases the access and the resilience of the system (Central Bank of the Bahamas, 2019, p.10).

In November 2021 (one year after the launch) the CBoB stated that there are more than $300,000 worth of Sand Dollars in circulation and 20,000 individuals (about 5% of the population) can access the Sand Dollar via mobile wallets (Robards, 2021).

Eastern Caribbean Currency Union (pilot)

The “DCash”-CBDC (DXCD) by the Eastern Caribbean Currency Union was the 2nd-launched central bank digital currency, even though the project is still officially in the pilot phase (ECCU, 2022). The pilot started in March 2021 following two years of development and testing with technology partner Bitt. DCash is available in seven of the eight insular state members of the ECCU with a population of about 600,000 people (UN, 2019 / DCash, 2022).

Motivation

According to the ECCU, the goals of issuing a CBDC are the following - “The objective of this pilot is to assess the potential efficiency and welfare gains that could be achieved: deeper financial inclusion, economic growth, resilience, and competitiveness in the ECCU - from the introduction of a digital sovereign currency.” (ECCU, 2022).

CBDC-Design

DCash is also a retail CBDC, available for customers on the DCash Wallet App. Customers are able to fund their wallets via financial institutions or paying “Merchant Tellers” with cash (DCash, 2022).

Financial institutions and approved service providers serve as intermediaries for registering and authenticating users. The DCash App has both transaction and holding limits, combined with a tiered KYC-process.

Technical background and CBDC-adoption

The ECCU has worked together with the technology provider Bitt since March 2019, developing a DLT-based system on Hyperledger Fabric (Bitt, 2019). At the end of the pilot project, DCash will be discontinued for the time being: "At the end of the pilot program, the ECCB will redeem and destroy the DCash balances. This will be tracked so we can easily audit how much has been destroyed and determine whether any DCash remains in circulation" (DCash FAQ, 2022). By the end of the first quarter of 2021, the ECCU reported about $400,000 (0.03% of money circulation) were issued in DCash (Straker, 2021).

On January 14th 2022, the ECCU reported a “Wide Service Interruption of DCash Platform […] caused by a technical issue and the subsequent necessity for additional upgrades” (ECCU Blog, 2022). The ECCU asserted, DCash balances stay unaffected, and transactions will be completed soon. On May 9th, the service was officially restored and the DCash platform was updated (DCash Facebook, 2022).

Nigeria

The e-Naira was officially launched by the Central Bank of Nigeria (CBN) in October 2021. The CBN has been investigating CBDCs since 2017 and the e-Naira was issued just four months after the announcement of the cooperation with technology provider Bitt (who had developed DCash for the ECCU) (CBN press release, 2021). Thus, the e-Naira is also built on Hyperledger Fabric.

Motivation

In the e-Naira design paper, the following motivations are listed towards a more efficient financial ecosystem (CBN, 2021a, p.iv):

- Improving the availability and usability of Central Bank money

- Supporting a resilient payment system ecosystem

- Encouraging financial inclusion

- Reducing the cost of processing cash

- Enabling direct welfare disbursements to citizens

- Increasing revenue and tax collection

- Facilitating Diaspora remittances

- Reducing the cost and improving the efficiency of cross-border payments

CBDC-Design

There are two apps provided by the Nigerian government, one for customers and one for merchants. The e-Naira employs a tiered KYC system with corresponding transaction and holding limits. Similar to the Bahamas and the ECCU, financial inclusion is an important motivation for issuing a CBDC for Nigeria as well. About 60% of 200 million Nigerians are unbanked, having no access to financial services (UN, 2019 / The World Bank, 2017). At the lowest KYC tier, the e-Naira requires just a verified telephone number. For higher tiers, customers need to verify credentials with their bank account. At the highest tier, users have a daily transaction limit of 500,000 e-Naira (~ $1,200) and a holding limit of 5 million e-Naira (~ $12,000) (CBN, 2021a, p.14). Registered merchants do not have holding or transaction limits.

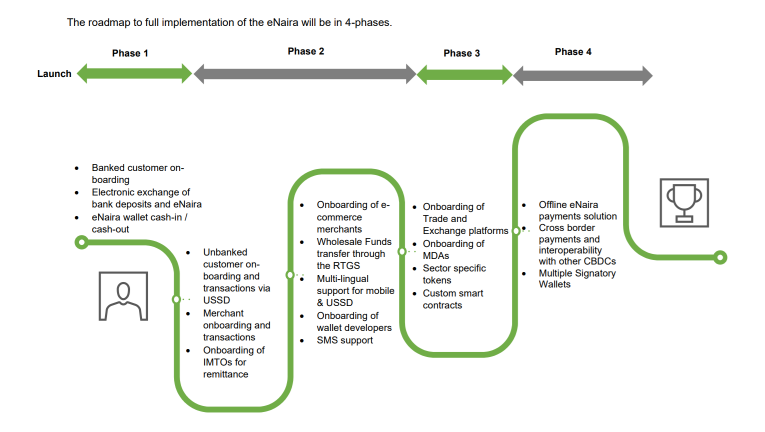

The CBN published “Regulatory Guidelines” for the e-Naira, focusing on compliance with AML/CFT as well as privacy and data protection (CBN 2021b). The e-Naira roll-out is planned in four phases (see figure 2 below); more functionalities are planned to be added over the next few years (offline-payments, cross-border transactions, custom smart contracts).

Figure 2

4 phase implementation (CBN, 2021a, p.21)

CBDC-adoption

Three weeks after the e-Naira launch, the central bank reported about half a million users generated a volume of 62 million naira ($150,000) in the app (Onu, 2021). This indicates that the e-Naira has many more users than the CBDC in the Bahamas or the ECCU. Relative to the population size of Nigeria however, this number of users is still very low. In a short poll by “African ventures” in February 2022, 64% of participants did not know of the e-Naira (Ogunjuyigbe, 2022).

Conclusion

Regarding CBDC-design, the three presented projects have many similarities, even though the motivation for issuing a CBDC is specific for every country. The Sand-Dollar (Bahamas), DCash (ECCU) and the e-Naira (Nigeria) have in common that they are retail CBDCs, focusing on the digital payment function on smartphones.

Due to the short period of time, the existing projects rather have basic functionalities. More “digital functions” like interoperability with other CBDCs, programmable payments for industry applications, offline-features, or cross-border payments, are something to come. In these cases, the infrastructure is provided by external companies, allowing the systems to be developed very fast. On the other hand, the DCash outage shows that outsourcing such important parts of the financial infrastructure can also be a risk.

The private sector (banks and other service providers) is involved in the CBDC process in all the examples, indicating that the digital central bank money is less about disintermediating banks, but working together and using existing infrastructure. To follow regulatory standards and manage the risks for the monetary system, the projects use a tiered KYC-system and transaction/holding limits. These limits are usually sufficient for everyday transactions, but not for large purchases. Hence, with regard to the diffusion of the presented CBDCs, the “digital money” seems to be an additional offer but is not comparable to diffusion of cash.

Recommendations for a Digital Euro

As has been highlighted, the differences among countries or jurisdictions in policy objectives, challenges, and concerns make it unlikely there is a standard approach to CBDC design. In the above case studies, the difference in the stages of economic development and sophistication of financial and payment systems it is clear that we cannot directly apply the lessons learned from the Bahamian Sand Dollar, the ECCU’s DCash, and Nigerian e-Naira to the digital euro.

While these three examples may be some of the only practical examples of large-scale retail CBDC implementation around the globe, they are still peculiar to their respective jurisdictions. The values transacted and number of users may not yet be systemic even in their respective economies.

Despite this general hesitation to extrapolate to the digital euro, perhaps one of the early conclusions of these three examples is that there are significant risks to creating a dependence on a single private sector service provider and their underlying technology or critical suppliers. DCash had an outage that lasted several weeks. Independent of its cause or blame, this may cause an unacceptable payment system disruption and reduce the confidence in and delay the success of a retail CBDC effort.

References

Atlantic Council CBDC Tracker (2021). Central Bank Digital Currency Tracker. https://www.atlanticcouncil.org/cbdctracker/

Bitt (20219). Bitt Develops World’s First Central Bank Digital Currency in a Currency Union. https://bitt.com/blog/bitt-develops-worlds-first-central-bank-digital-currency-in-a-currency-union/

Boar, C., Wehrli, A. (2021). Ready, steady, go? – Results of the third BIS survey on central bank digital currency. BIS Papers, No. 114, https://www.bis.org/publ/bppdf/bispap114.pdf

CBDC Tracker (2021). Today's Central Bank Digital Currencies Status. https://cbdctracker.org/

CBN (2021a). DESIGN PAPER FOR THE eNAIRA. https://enaira.com/download/eNaira_Design_Paper.pdf

CBN (2022b). REGULATORY GUIDELINES ON THE eNAIRA. https://www.cbn.gov.ng/Out/2021/FPRD/eNairaCircularAndGuidelines%20FINAL.pdf

CBN press release (2021). CBN Selects Technical Partner For Digital Currency Project. https://www.cbn.gov.ng/Out/2021/CCD/CBN%20Press%20Release%20(CBDC)%2030082021.pdf

Cemla Fintech Forum (2020). Implementing a CBDC: Lessons Learnt and Key Insights Policy Report. Central Bank Digital Currencies Working Group (CBDC WG). https://www.cemla.org/fintech/docs/2020-Implementing-CBDC.pdf

Central Bank of the Bahamas (2019). PROJECT SANDDOLLAR: A Bahamian Payments System Modernization Initiative. https://www.centralbankbahamas.com/publications/main-publications/project-sanddollar-a-bahamian-payments-system-modernization-initiative

Chen, S, Goel, T, Qiu, H and Shim, I (2022). BIS Monetary and Economic Department. CBDCs in emerging market economies. BIS papers No 123, p. 1-22. https://www.bis.org/publ/bppdf/bispap123.pdf

DCash (2022). The future of the EC currency is digital!. https://www.dcashec.com/; https://www.dcashec.com/faqs/the-projec

DCash Facebook (2022). DCash EC. https://www.facebook.com/DCashECCU/

Eastern Carribiean Central Bank (2022). About the Project. https://eccb-centralbank.org/p/about-the-project

ECCU Blog (2022). Region-Wide Service Interruption of DCash Platform. https://www.eccb-centralbank.org/news/view/region-wide-service-interruption-of-dcash-platform

eNaira (2022). Same Naira. More Possibilities. https://www.enaira.gov.ng/, https://www.enaira.gov.ng/about/faq

Mastercard (2021). Mastercard and Island Pay launch world’s first central bank digital currency-linked card. https://www.mastercard.com/news/press/2021/february/mastercard-and-island-pay-launch-world-s-first-central-bank-digital-currency-linked-card/#:~:text=Under%20a%20new%20program%20from,Islands%20and%20around%20the%20world

NZIA (2019). NZIA Limited Identified as Preferred Technology Solutions Provider by the Central Bank of The Bahamas for Digital Currency Project. https://nzia.io/pr/central-bank-of-the-bahamas/

Ogunjuyigbe, O. (2022). WHY DOES THE E-NAIRA HAVE SO LITTLE ADOPTION?. https://venturesafrica.com/why-does-the-e-naira-have-so-little-adoption/

Onu, E. (2021). Nigeria’s E-Naira Lures About Half a Million People Weeks After Its Launch. Bloomberg. https://www.bloomberg.com/news/articles/2021-11-15/e-naira-lures-about-half-a-million-people-weeks-after-its-launch

Robards, C. (2021). Sand Dollar circulation grows but spend still low. The Nassau Guardian. https://thenassauguardian.com/sand-dollar-circulation-grows-but-spend-still-low/

Sand Dollar (2022). Digital Bahamian Dollar - Inclusive | Convenient | Secure. https://www.sanddollar.bs/; https://www.sanddollar.bs/legalframework

Straker, L. (2021). Banknotes are most used currency in ECCU. Grenada News. https://www.nowgrenada.com/2021/07/banknotes-are-most-used-currency-in-eccb/

The world bank (2017). Global Findex database. Indicator table. https://globalfindex.worldbank.org/sites/globalfindex/files/2018-04/2017%20Findex%20full%20report_indicator%20table.pdf

United Nations (2019). Department of Economic and Social Affairs. World population prospects 2019. https://population.un.org/wpp/Download/Standard/Population/

This article was prepared by the authors. The views expressed in this article are the authors' own and do not necessarily reflect the views of the Digital Euro Association.

No Comments Yet

Let us know what you think