Share this

by Digital Euro Association on Sep 28, 2022 11:31:31 AM

Authors - Dr. Jochen Biedermann and Juan Gutierrez.

This is the second article in our Public Digital Euro Working Group series. The objective of this article is to provide an updated perspective on the e-CNY (aka e-RMB, Digital Yuan, Digital Renminbi - the Chinese CBDC) for those already familiar with CBDCs. The focus will be on the practical lessons from live and ongoing pilots, rather than a theoretical or taxonomic discussion.

The following section provides some background into China’s payment system. The third section centers around the extended pilot of the digital yuan while the article closes with specific recommendations for the Digital Euro, based on lessons learned from the e-CNY, its structure and implementation.

Background

Mobile payments have been popular in China and their adoption has likely increased with the pandemic. In 2019 alone, 64% of payments for personal consumption were mobile payments, and Chinese consumers used mobile payment on average 3.25 times a day, as stated in the China UnionPay 2019 Mobile Payment Report. Almost 58% of the Chinese population used mobile payments in 2020. [Source: 46th Statistical Report on Internet Development in China - CNNIC] and cash use is in significant decline.

Two private payment networks play a dominant role in mobile payments: Alipay by Ant, based in Hangzhou, and WeChat Pay (or Tenpay) by Tencent, based in Shenzhen. Both have created complete ecosystems for all kinds of financial transactions as walled gardens, making it rather costly to move money outside of these ecosystems. Both have more than 900 million active users [Source: Statista] Regulatory action against Ant in 2020/2021 and more recently against Tencent has underlined an increasing concern by the Chinese government and at the People’s Bank of China (PBoC) about the systemic relevance of both providers, and how these private money issuers could impact wider public policy objectives.

By issuing e-CNY and forcing interoperability with the aforementioned private payment networks, PBoC and the Chinese government seem to plan to reduce consumer lock-in and regain control over domestic retail payments, including keeping the central bank at the core of money in an increasingly digital China.

In summary, some may question the need for the PBoC and its government to introduce a digital yuan in what is arguably already one of the most advanced retail payment ecosystems and one that is already highly integrated into its digital economy.

In the next section we will outline how authorities and regulators seem to have concluded, only a few years after granting payment licenses to non-bank providers, that there is still a need for a digital yuan.

China’s long running CBDC pilot

e-CNY is the longest-running and most advanced large-scale CBDC pilot globally. The PBoC’s Digital Currency / Electronic Payment (DC/EP) project arguably started as early as 2014. (Figure 1)

Source: Dingxin Gao

The Digital Currency Research Institute was created in 2016 as the PBoC’s formal research body for the development of digital currencies and blockchain technology and it continues to play a role in the pilot and payment system development in China.

In parallel to these digital yuan efforts, the Chinese government, like others around the world, could not ignore cryptocurrencies and their potential impact on payments, financial stability and cross-border transactions. China restricted crypto trading during the 2017 crypto bull market and more recently restricted other crypto-related activities such as cryptocurrency mining. It could be said that China has applied some of the most restrictive policies on cryptocurrencies to maintain its capital controls.

There have been many publications on the digital yuan over the years, but perhaps the most complete and relevant publication is that published by the PBoC’s Working Group on e-CNY Research and Development whitepaper in July 2021. In it, the working group states that the e-CNY objectives are:

- “to diversify the forms of cash provided to the public, satisfy the public’s demand for digital cash and support financial inclusion”

- “to support fair competition, efficiency and safety of retail payment services”

- “to explore the improvements of cross-border payments”

The Working Group describes the e-CNY as follows:

“Firstly, e-CNY has all the basic functions of money, i.e., unit of account, medium of exchange, and store of value. Same as the physical form of RMB, e-CNY is China’s legal tender. Secondly, e-CNY is the digital version of China’s fiat currency. Throughout history, the form of currency has evolved from objects, metal coins to banknotes. Such evolution of currency is a result of progress made in science and technology as well as evolution of economic activities. The issuance and circulation of e-CNY is identical with physical RMB, while the value of the former is transferred in a digital form. Thirdly, e-CNY is the central bank’s liabilities to the public. Backed by sovereign credit, e-CNY has the status of legal tender. (...) The e-CNY is a substitute for M0. Thus, it is treated the same as the physical RMB under M0, which carries and pays no interest.”

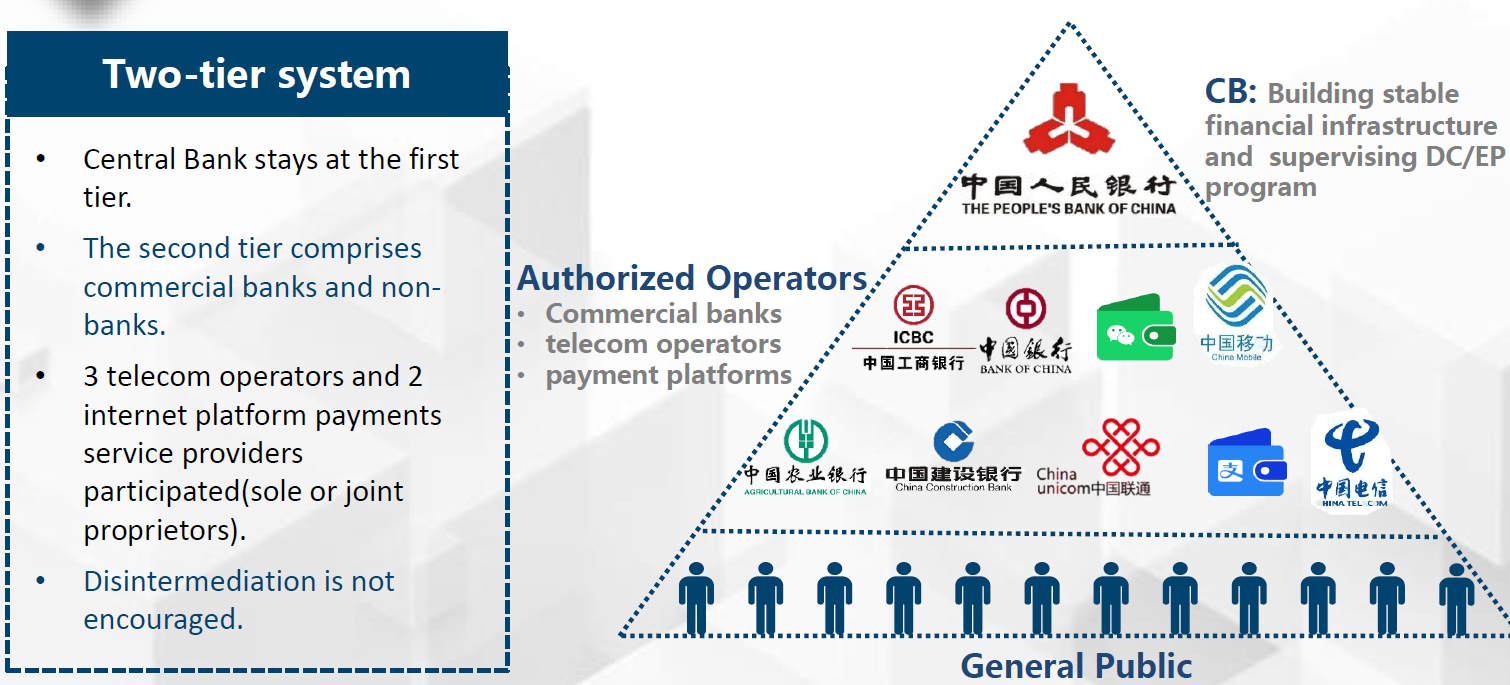

The e-CNY is based on a two-tier, multi-scheme structure. The first tier connects the PBoC with banks, telecom operators and the large scale payment networks (“Authorized Operators”). Those operators offer e-CNY to retail clients in the second tier (Figure 2). It should be noted that this pilot was not restricted to banks, nor to the two payment platforms. Pilots seem to have included all private sector participants that have been issuers or significant intermediaries for digital money, including telecom operators. The central bank has retained issuance, control of the infrastructure, and supervision, but provided a allowance for several types of intermediaries, not just traditional financial institutions.

Source: Dingxin Gao

The PBoC has declared that it will not mandate a certain form for the e-CNY but remain neutral on technology. The e-CNY might be offered as an account-based e-wallet, as a QR code (the most popular form of payments in China), as NFC payment (e.g., Apple/Huawei/Samsung Pay), as bank card/plastic card - online or as pre-paid accounts/cards for offline payments. Furthermore, the PBoC has stressed that using decentralized technology is not a key priority.

To balance KYC & privacy, the PBoC has designed different account levels, including two types of anonymous wallets, that is that don’t require an ID card:

Source: Alex Lew on Medium

The Chinese government has mandated that all merchants who accept digital payments (e.g., Alipay and WeChat Pay) have to accept the e-CNY.

The e-CNY offers dual offline payments. If both parties of the transaction have an e-CNY digital wallet installed on their mobile phones, they can transfer money even without network access and bank accounts. To enable dual offline payments, PBoC uses loosely coupled account links for achieving “controllable anonymity”.

While there hasn’t been a formal analysis of the legal framework, the previously cited description of the digital yuan seems to stress an equivalence to a physical yuan, perhaps indicating that its extension of the central bank’s existing mandate: “The issuance and circulation of e-CNY is identical with physical RMB, while the value of the former is transferred in a digital form. Thirdly, e-CNY is the central bank’s liabilities to the public. Backed by sovereign credit, e-CNY has the status of legal tender. (...) The e-CNY is a substitute for M0.

The test phase of the DC/EP project started in April 2020, initially in the Chinese cities of Shenzhen, Suzhou, Chengdu, and Xiong’an. The early tests were supported by free giveaways of e-CNY. For instance, in Shenzhen, 10 million e-CNY was distributed in the form of 50,000 digital red envelopes during a week in October 2020. By associating these early tests to an established tradition, the pilot sought to capitalize on established networks. It probably also reduced the negative association to legal tender if the pilots were not successful. PBoC has extended the tests to Shanghai, Hainan, Changsha, Xi'an, Qingdao, Dalian, Beijing, and other places during 2021. The pilots have also included different types of offline and online commerce and payment functionality. The digital yuan has thus been extensively and carefully tested in many controlled experiments.

As of June 2021, the Agricultural Bank of China and ICBC had offered more than 3,000 e-CNY-to-Cash ATMs in Beijing. [Source: Xinhua Finance, “ATM机上能取数字人民币”].

At the end of 2021, 261 million personal e-CNY-wallets had been opened, and the total e-CNY transaction amount had reached 87.6 billion yuan (almost 13 billion €). [Source: State Council Information Office press conference on financial statistics, January 2022]

The PBoC announced that they are going to expand the digital yuan’s area of application pilot to the rest of China’s respective provinces. These include Shenzhen in Guangdong Province, Suzhou in Jiangsu Province, Xiongan New Area in Hebei Province, and Chengdu in Southwest China’s Sichuan Province.

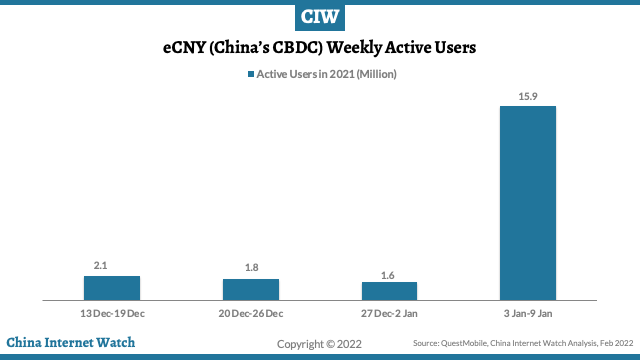

The number of e-CNY weekly active users increased to almost 16 million in the first week of 2022 and the total number of unique users totaled 261 million at the end of 2021.

Source: China Internet Watch

These numbers vastly exceed the pilots or go-lives of the Bahamas, Eastern Caribbean, and Nigeria and would probably be considered a successful go-live of a new payment system in many countries based on the sheer number of users and transactions.

For a couple of years there had been speculation that the official launch of the digital yuan would occur in the Winter Olympics of 2022. Given the Covid-19 pandemic and the reduced attendance and attention the Winter Olympics received, the e-cny’s use at the Winter Olympics seems to have been considered merely another pilot in the wider effort.

Foreign visitors to the Winter Olympics were able to use the e-CNY either through the e-CNY mobile phone app or a hardware wallet. Such hardware wallets were already presented at the 2021 China International Fair for Trade in Services (CIFTIS) in September 2021. This is not the first consideration of offline use of the digital yuan in the pilot and this capability will likely continue.

Source: China Daily

A video of the app showed the use of the digital yuan to pay for grocery items associated with the Winter Olympics, confirming at least the basic functionality in a live setting. [Source: Coindesk]

A more detailed review of the app walks through various aspects, such as the capacity to deposit and transfer to bank accounts without leaving the app, and details of the underlying digital yuan token, perhaps confirming it is a central bank liability even if it is used through private authorized operators. [Source: Richard Turrin ]

Although there have been repeated mentions of its local focus, the PBoC has started to test the cross-border use of the e-CNY. In April 2021, the use of e-CNY wallets was explored in Hong Kong, and in June 2021, e-CNY connectivity to the Hong Kong Monetary Authority (HKMA) domestic payment systems was tested. [Source: Reuters].

Additionally, in February 2021, the HKMA issued a Joint statement on Multiple Central Bank Digital Currency (m-CBDC) Bridge Project:

“The HKMA, together with the Bank of Thailand (BOT), the Central Bank of the United Arab Emirates (CBUAE) and the Digital Currency Institute of the PBoC (PBoC DCI), announced the joining of the CBUAE and the PBoC DCI to the second phase of Project Inthanon-LionRock, a CBDC project for cross-border payments initiated by the HKMA and the BOT. This joint effort is strongly supported by the Bank for International Settlements Innovation Hub Centre in Hong Kong and the project has been renamed as ‘Multiple Central Bank Digital Currency (m-CBDC) Bridge.’ Building on the experience learnt from Project Inthanon-LionRock, the m-CBDC Bridge Project will further explore the capabilities of distributed ledger technology (DLT), through developing a proof-of-concept (PoC) prototype, to facilitate real-time cross-border foreign exchange payment-versus-payment transactions in a multi-jurisdictional context and on a 24/7 basis. The m-CBDC Bridge Project will also explore business use cases in a cross-border context using both domestic and foreign currencies.”

Conclusions

Given the crucial role of authorized operators and their advanced digital offerings some may question if the digital yuan is formally a CBDC. They may argue that the Authorized Operators custody e-CNY balances, control its technology and system, and are responsible for compliance and data privacy of the retail users. In this argument, the PBoC supervises the e-CNY, provides the clearing & settlement infrastructure, and promotes & enforces interoperability between the different payment solutions of the operators. Without getting into a detailed discussion on the boundaries between a CBDCs and e-money or even a stablecoins, in practice, the digital yuan is a CBDC because it is explicitly a central bank liability equivalent to cash, and this can even be verified in the app through the mentioned underlying token.

The first conclusion of the digital yuan is that it has been successful by most metrics. The central bank created a formal working group, carefully designed varied pilots in several regions that gradually increased their payment functionality and slowly integrated different types of intermediaries over several years. The pilot has already reached a significant portion of the population and more than a million merchants. There has been an integration of the e-CNY into the existing payment infrastructure, through both the e-CNY app, hardware wallets, and addressing specific needs or services. There has been a gaining of momentum and trust of the population.

Despite these positive developments from the extensive pilot, there has been no official launch set for the digital yuan and it is not clear what the criteria to be met are. The successful go-live of the digital yuan is also not guaranteed, among other challenges, because it has been reported that a portion of users have not found a unique proposition for it compared to the other forms of digital money that they have already been using extensively.

Specific Recommendations for the Digital Euro

The PBoC has tailored the e-CNY and its pilots to the very specific and highly advanced mobile payment landscape in China. That may limit how much can be transferred directly as a recommendation from the digital yuan's extended and relatively successful pilot.

Considering the high centralization of several aspects of the Chinese economy it is relevant that PBoC has chosen a two tier structure and privacy tiers. The two-tier structure retains the central bank control of regulation, issuance, interoperability and payment system but it gives a clear role to existing private payments service providers, that is banks, telecom operators and payment platforms such as Alipay and WeChat Pay/TenPay. The decision to interconnect these two dominant private payment ecosystems and seek parity in merchant acceptance, may be a clear advantage over the previous walled garden approach.

China likely provides a lesson on how long it takes to diligently expand a pilot. A task force was created in 2014, an institute was created in 2016, pilots have now covered hundreds of millions of users and more than a million merchants in several regions. These tests have taken years and are already at a scale that would be successful for almost any new payment system. The digital euro therefore seems to be on the correct path by establishing a relatively long timeline for the introduction of this new form of public money. The eurozone may have an even greater challenge given the diversity of its payment infrastructure and underlying legal, technological, and cross-border frameworks.

While the international or geostrategic aspects of the e-CNY might have been exaggerated before the invasion of Ukraine, they may be gaining more relevance now. That said, the e-CNY is mainly designed for local retail purposes and no significant role has been detected in the pilots to reduce potential financial sanction pressure.

Sooner or later China might want to distribute the e-CNY internationally, particularly, alongside its “Belt & Road Initiative (BRI).” Citizens of the countries targeted by the BRI might use the e-CNY via mobile wallets, bypassing international payment infrastructure like SWIFT and the credit card schemes. The international spillovers of a successful live digital yuan which is used by other countries deserves continued attention.

Download the article here

This article was prepared by the authors. The views expressed in this article are the author’s own and do not necessarily reflect the views of the Digital Euro Association.

No Comments Yet

Let us know what you think